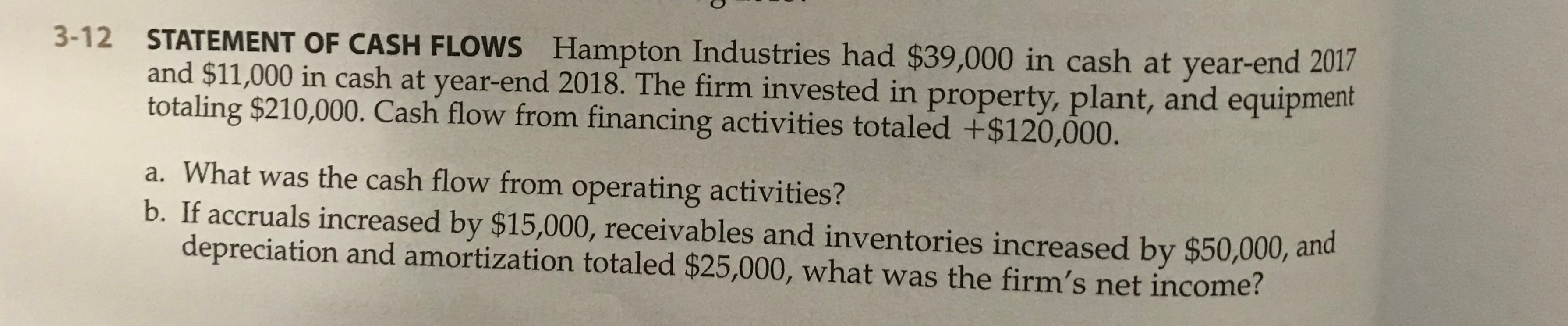

Whatever they may offer instead is actually the next financing to pay for the 3 % and you can complete the latest gap

The benefit of the fresh FHA mortgage ‘s the far less down percentage requisite and lower expenses associated with home loan insurance policies. If you find yourself nevertheless necessary, they are both far faster and less out of pocket towards debtor than the average field options.

The brand new downside of FHA loan is the fact that the functions qualified as thought have to be underneath the FHA value accounts. The FHA mortgage system isnt available for all household to the the marketplace, and will rule out extreme areas of California where in actuality the average home price is large.

Possess Zero Advance payment having a ca Grant Program

Various Ca give applications exists to aid overcome otherwise entirely safeguards down payment costs for buyers, eg very first time homeowners. Listed here is an inventory for only California features:

Traditional 97% LTV Mortgage

The personal markets choice for a no or low down-fee pick is basically the mortgage-to-Worth (LTV) Mortgage alternative. It www.cashadvancecompass.com/installment-loans-fl/san-antonio is an exclusive lender automobile that’s not made available from all of the bank resource house transformation. It’s really worth deciding on, however, since the real down-payment needs are a decreased step 3 percent of total purchase value.

That is Qualified to receive a conventional 97% LTV Financial?

Qualified consumers generally were individuals with debt lower than 41 % of money, a pretty a good credit score rating more than 620, zero prior owning a home in the last 36 months, number 1 residence intent to the possessions getting ordered, plus the complete investment are 97 % limitation.

What are the Criteria?

In the course of time, new borrower must assembled step three % of marketing getting a down payment. * There is absolutely no LTV zero-deposit financing inside system, also certainly one of individual lenders. The debtor after that works out that have one or two loan costs because a beneficial effect. The buyer also needs to end up being a first-go out home buyer, and the assets have to be one family home simply.

Exactly what are the Charges?

There clearly was a private home loan insurance coverage component. It does start around 0.75 to one.25 percent of your buy worth and can be distributed month-to-month in the loan. * There are also settlement costs normal of one’s business.

Pros and cons away from Conventional 97% LTV Mortgage

An advantageous asset of the personal business LTV mortgage is that here isn’t any upfront charge to have personal mortgage insurance policies, and when equity reaches twenty two per cent the insurance cancels. The fresh new deposit needs is 3 %, even less than the FHA comparative requisite. Therefore the large in addition to ‘s the highest financing wide variety it is possible to in which regulators programs was capped.

Brand new downside of LTV loan is actually a very conservative financing so you can earnings need for consumers. Oftentimes, manufacturers you will need to assist, however with an enthusiastic LTV financing, he could be limited to step 3 percent. College loans in deferment can be counted because the financial obligation in which inside regulators software he could be ignored. And finally, the financing get lowest exceeds bodies applications.

Just how to Cover Closing costs

Even with a loan recognition, a california homebuyer often nevertheless score struck that have settlement costs that variety anywhere from $2,100000 to help you $ten,100 inside the a buy. Far utilizes the fresh offered sale and requirements wanted to. You can find about three larger implies for a borrower to cover closing can cost you beyond getting more income and saving alot more ahead of the acquisition. Talking about gifts, financial credits otherwise vendor loans.

Provide Financing

Aside from the maximum from taxation for the gifts you to definitely hit the giver, current money also are restricted to a level to be certain the actual visitors of a home is involved in the get. Since the a loan provider has actually regulators requirements to determine all the money present within the a sale, the latest provide giver will most likely must offer certification of one’s loans, the resource, their mission and you may courtroom degree of your present. As opposed to so it, money cannot be put. Providing a present is not as simple as applying $10,one hundred thousand to an advance payment out of a present from Cousin Fred out of nowhere. Next, certain applications wanted that a down payment end up being a mixture of provide and personal financing, never assume all current loans.